Position sizing refers to the number of shares, contracts, or units of an asset that an investor decides to buy or sell in a specific trade when a position opening signal is triggered. In other words, it is the amount of capital that an investor is willing to risk on a trade based on their strategy and risk tolerance level.

An optimal position sizing strategy is a crucial component of algorithmic trading, addressing questions such as:

-

When a position opening signal is triggered, how much capital should be allocated? More specifically, should the entire capital be invested in a single trade, or should it be divided into several portions to participate in multiple trades at different times when position opening signals occur?

-

If the capital is divided into several portions, what percentage of capital should be allocated to each trading signal?

When developing a trading algorithm, determining the optimal position sizing strategy and the asset allocation strategy are two inseparable components, both related to the management and utilization of capital. These strategies differ in terms of timing. The optimal position sizing strategy specifies how much capital is allocated to each trade at different times when position opening signals occur, while the asset allocation strategy determines the percentage of capital allocated to each type of security at a given position opening.

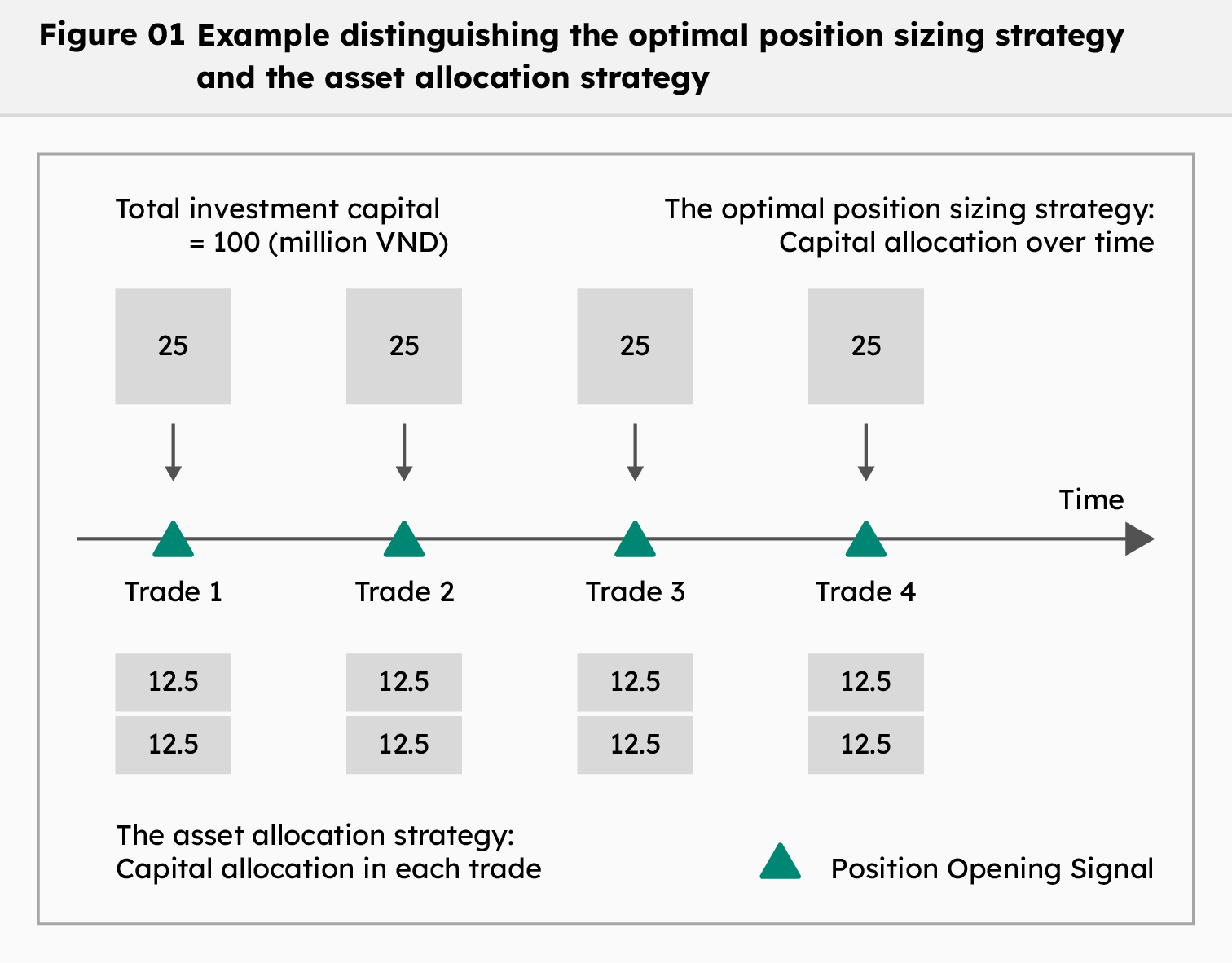

The following is an example that distinguishes the optimal position sizing strategy and the asset allocation strategy.

An algorithmic trader has developed a set of criteria to evaluate the strength of stocks. With a capital of 100 million VND, the trader applies a strategy of gradually opening buy positions over 4 consecutive days, rather than investing the entire capital at once. Specifically, each day, 25 million VND (¼ of the total capital) is used to buy the 2 stocks rated strongest based on the established criteria, with each stock allocated 12.5 million VND.

The optimal position sizing strategy is clearly demonstrated by dividing the capital to open positions at four different points in time. The asset allocation strategy is reflected in how, at each position opening signal, the capital is equally allocated to two different stocks, following an equal weighting method.

Why Divide Position Sizing?

Instead of investing 100% of the capital in a single trade, dividing position sizing offers the following benefits:

-

Risk reduction. Rather than committing all capital in a single trade, dividing the position size helps minimize potential losses if the trade is unsuccessful. This is especially important in highly volatile stock markets with many unpredictable factors. A series of consecutive losses could lead to “blowing up" the account if the position size is too large. Splitting the position helps to protect the investor’s capital and ensures that the investor can continue participating in the market.

-

Leveraging the law of large numbers. Dividing the position size indirectly increases the number of trades, thereby leveraging the law of large numbers. According to this principle, as the number of trades increases sufficiently, the actual average result will converge toward the theoretical average (expected) value. In other words, if a trading strategy has a higher probability of winning than losing, executing more trades increases the likelihood of achieving overall positive and more stable profits in the long term.

-

Adapting to market liquidity conditions. In practice, there aren't always numerous opportunities to open positions at ideal prices. In markets with relatively low trading liquidity compared to the capital size, the trading algorithm needs to adapt flexibly by using a small portion of the capital to open a position and then continue to wait for the next position opening signals.

In summary, the strategy of dividing position size not only helps minimize risk and optimize profits but also provides flexibility in capital management for trading algorithms, especially in volatile markets or when there are fewer attractive trading opportunities.

Optimal Position Sizing Strategies

Below are some popular optimal position sizing strategies:

-

Fixed-volume position sizing. Buy or sell a fixed number of shares or contracts for each position opening signal, regardless of price or market conditions.

-

Percentage-of-capital position sizing. Allocate a fixed percentage of total capital for each position opening signal.

-

Signal confidence-based position sizing. Adjust the position size based on the confidence level or probability of success of each trading signal. The idea behind this strategy is to invest more in trades with a higher likelihood of profitability and less in trades with higher risk. An example of this approach is the Kelly Criterion. This mathematical formula calculates the optimal position size based on the probability of winning and the ratio between the average profits when winning and the average loss when losing. For more information on the Kelly Criterion, refer to the article: Kelly Criterion - Definition and Application.

There is no single optimal position sizing strategy that is perfect and suitable for everyone. Traders need to experiment, evaluate, and continuously adjust to find the optimal position sizing strategy. Combining theoretical knowledge, practical experience, and flexibility in application will help traders achieve success in the highly volatile financial markets.

Conclusion

Position sizing plays a crucial role in algorithmic trading. Choosing the appropriate optimal position sizing strategy requires not only an understanding of fundamental principles like the law of large numbers but also careful consideration of trading style, risk tolerance, and the unique characteristics of each investment strategy.

Finally, it is important to note that position sizing is just one component of a complete trading algorithm. To achieve success in algorithmic trading, traders need to develop a comprehensive process that includes other key elements such as stock selection strategy, determination of entry/exit points, and execution strategy.